EuroSite Power (EUSP)

MC: $3.12M

EV: $0.54M

Summary

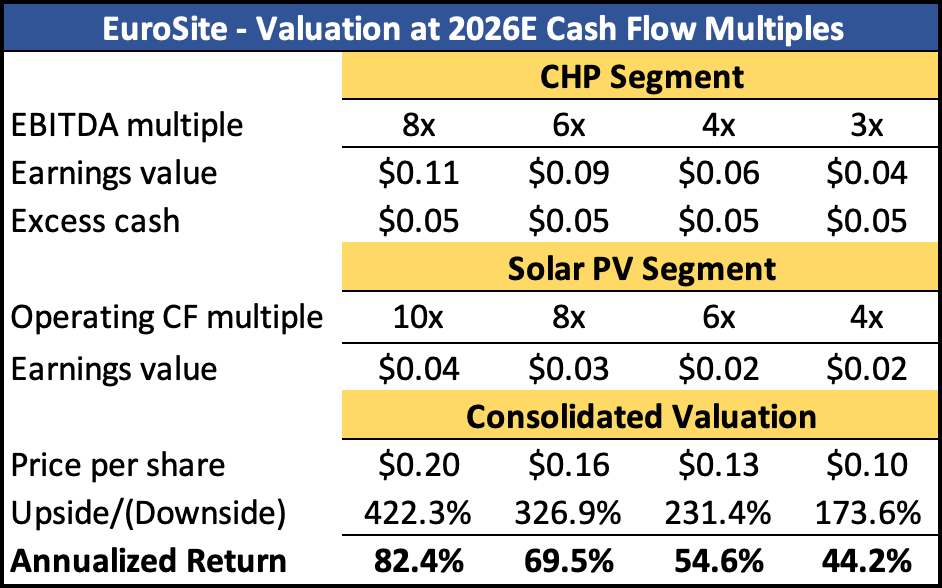

EuroSite Power (EUSP) is a completely obscure, little utility company that is priced at scrap value. Revenue, which is guaranteed under long-term contracts, has grown at a 22% CAGR since 2015. Last year, management created a new solar PV product segment that could be worth more than the current market cap in 2-3 years. Despite this, the stock trades at <2x LTM EV/FCF, and at roughly half the price that it traded at 4 years ago when it had 60% less revenue and was unprofitable. Our estimated value of the CHP and solar PV segments, based on our 2026 estimates, uses a 6x EV/EBITDA multiple and an 8x EV/Operating Cash Flow multiple. This equates to a $0.16 per share value, which is ~327% above the current bid of $0.038.

Overview

EuroSite Power distributes, installs, and maintains combined heat and power (CHP) units for small-scale facilities in the UK. The use cases of CHPs arise from the inadequacies of sourcing electricity from the grid (also referred to as ‘centralized power generation’). Centralized power generation loses 50-70% of generated electricity to waste heat, transportation, and distribution processes, etc. resulting in plant efficiency rates of 30-50%. CHP, essentially an on-site gas-fired electricity generator with a heat recovery system, is able to save and then sell what would otherwise be waste heat, reporting generator efficiencies of 75-92% as a result (example below).

EuroSite provides an alternative option for financing and maintaining CHP systems for small-scale facilities through what are basically floating-rate power purchase agreements (PPAs). In this model, EuroSite maintains ownership of the system, installs it into the customer’s facility, and is responsible for maintenance and repairs. In exchange, the customer signs a 10-15 year agreement to buy all electricity and heat produced by the unit at a rate-adjusting 5-15% discount to grid prices (centralized power rates). Because of the efficiency gap between CHP systems and centralized power generators, EuroSite can mark up the electricity it produces by 35-45% of the cost and still deliver savings to customers.

Regarding unit economics, EuroSite’s revenue is indexed to prevailing electricity prices, with gross margins tied to the difference between the price at which it can sell a kW of electricity and the cost of the natural gas required to produce it (termed the ‘spark spread’). The UK spark spread has widened almost every year since 2015, largely due to intense government regulation of carbon-producing plants (both coal & gas) causing a decrease in their demand for natural gas and supply of electricity – without a proportional decrease in European consumption. This has resulted in somewhat consistent 0.5-2.0% annual gross margin improvements. Spark spread compression is expected to occur through the next fiscal year, though the long-term trend of improvement does not show signs of reversing.

History & Management

EuroSite was created as a subsidiary of American DG Energy in 2014 and was floated on the public market in 2016. Its purpose: to bring American DG’s on-site CHP model to the UK. By 2016, though the management had created $1.8M in recurring sales from scratch, the company was burning an enormous amount of cash every year. American DG then recapitalized the company and replaced the then-CEO with American DG Director, MIT graduate, and former Columbia University professor, Elias Samaras, who has been the CEO since. Both Samaras and COO Paul Hamblyn, who seems to be in charge of the day-to-day operations and investor relations, have a strong academic and professional background in P&U and renewables generally.

Samaras executed an intense cost-cutting program in 2016, which included delisting the stock from the NASDAQ and significantly reducing reporting. The company then grew its CHP operations well until 2020 when the pandemic forced its customers to shut down operations. It has since had issues returning to its ~59k MWh 2019 peak.

The board is made up of six members, of which Samaras is one, with a combined ownership of ~27% of the company stock. The Chairman, Jacques de Saussure, is a retired Partner of the Pictet Group, and is the descendant of the well-known de Saussure Swiss banking family. His involvement, along with Brevan Howard co-founder and portfolio manager Trifon Natsis, who owns ~35% of the company alone, means that poor capital allocation should not be an issue in the future.

Solar PV Segment

Late in 2023, EuroSite announced the creation of a renewables subsidiary. It has since hired a Sales Director, Matthew Briddle, to lead the new arm. In ~8 months, EuroSite has 27 contracts with a total capacity of 8700 kWe in backlog. Not all 27 will convert but over the negotiation and installation phases, they will be finding new contracts, which should allow them to sign and convert the equivalent of 27 contracts by then, if not more.

Management estimates a 9-12 month range from the signing of the term sheet to construction completion. Negotiation of the term sheet can take up to 3-6 months, suggesting that the contracts in backlog could be fully constructed in 1-1.5 years.

We have estimated the potential financial profile of these 27 contracts, using live PV Output trackers in three of the more economically sensible areas of the UK for these systems to be built. Because the solar PV segment follows the same floating-rate PPA structure as the CHP segment, we have included a 10% average discount to grid rates in our revenue calculations.

All example PVs have been running for at least 400 days, meaning that seasonality is accounted for in their output figures. It should be noted that these PVs, especially the West Midlands and South West PVs, could be off due to the difference in size—though the closeness in production estimates between the three regions is reassuring.

The following operating cash flow estimate averages the financials of the three examples above to create a hypothetical picture of the overall segment. Management has an agreement with several region lenders for “100% project funding based on an asset backed, receivables type arrangement”. We have estimated a 10% interest rate, which at 465 bps above SOFR we believe is conservative, on the estimated total CapEx of $11.1M. Unfortunately, the need to service these various projects simultaneously requires a large working capital balance as the project funding is only received after the construction completion.

The growth of the solar PV segment is an important catalyst for the revaluation of the company considering most American comps trade deep in the double digit EV/EBITDA multiples.

CHP Segment

Below we have estimated EuroSite’s cash flow over the next three years. Projected avg. MWh prices have been taken directly from the futures market for the given years and repriced using an 11.7% annual risk premium. Additionally, the MWh prices are discounted by 6% to reflect the customer grid price discount. It should also be noted that, according to management, the average length left on one of EuroSite’s CHP contracts is 8.4 years, meaning that the firm has strong staying power.

Management has claimed that it will deliver revenue higher in FY 2024 than in 2023. I believe that management is either including the rapid implementation of the PV segment, or the completion of the few CHP projects in backlog. Otherwise, these expectations seem greatly overoptimistic — which management doesn’t have a history of being, except before great downturns (ex. ‘18/’19).

Valuation

Catalysts

The working capital constraints of the PV segment necessitate a sizeable cash balance. As the economics of the PV segment currently stand, it doesn’t make sense to siphon cash away from this high-return segment. However, when it is timely to return cash to shareholders, we believe the board will recognize this and deliver.

Takeover

CHP assets are well-regarded in the portfolios of large-scale utility companies and infrastructure private equity shops. Based on precedent transactions, we believe that EuroSite’s locations could be acquired by a strategic for $10M - $15M, which alone represents 2x - 3x the current market cap. Tecogen, now the parent company of American DG Energy, has had a history of selling off individual locations, which, if anything, ensures liquidity for EuroSite and possible realization of the CHP assets’ value without a complete sale of the segment.

Uplisting

An uplist to the OTCQX could create volume sufficient to unlock shares that are currently closely held. In the medium term, the stock will likely remain highly illiquid due to the high ownership concentration. However, the float, ~30% of the s/o, should still be sufficient to create price discovery assuming enough investor demand. Including the fees to uplist, the all-in expenses would likely not be much more than the directors’ $200,000 compensation.

Your write-ups are high quality, appreciate the work. Great find. Looks very volitale though as it is very small. Looks like a dream stock for swing traders during the last 3 years. I don't have much experience with such small companies. Are there not bigger fraud risks, etc? What other risks do you see that would kill the thesis? Cheers